Fighting Friendly Fraud: A Revenue Recovery Strategy

A new solution helps deal with a growing problem

Faceless hackers may dominate the headlines, but they are not always the biggest financial threat to businesses. In reality, by far the greatest financial impact comes from customers who simply change their minds.

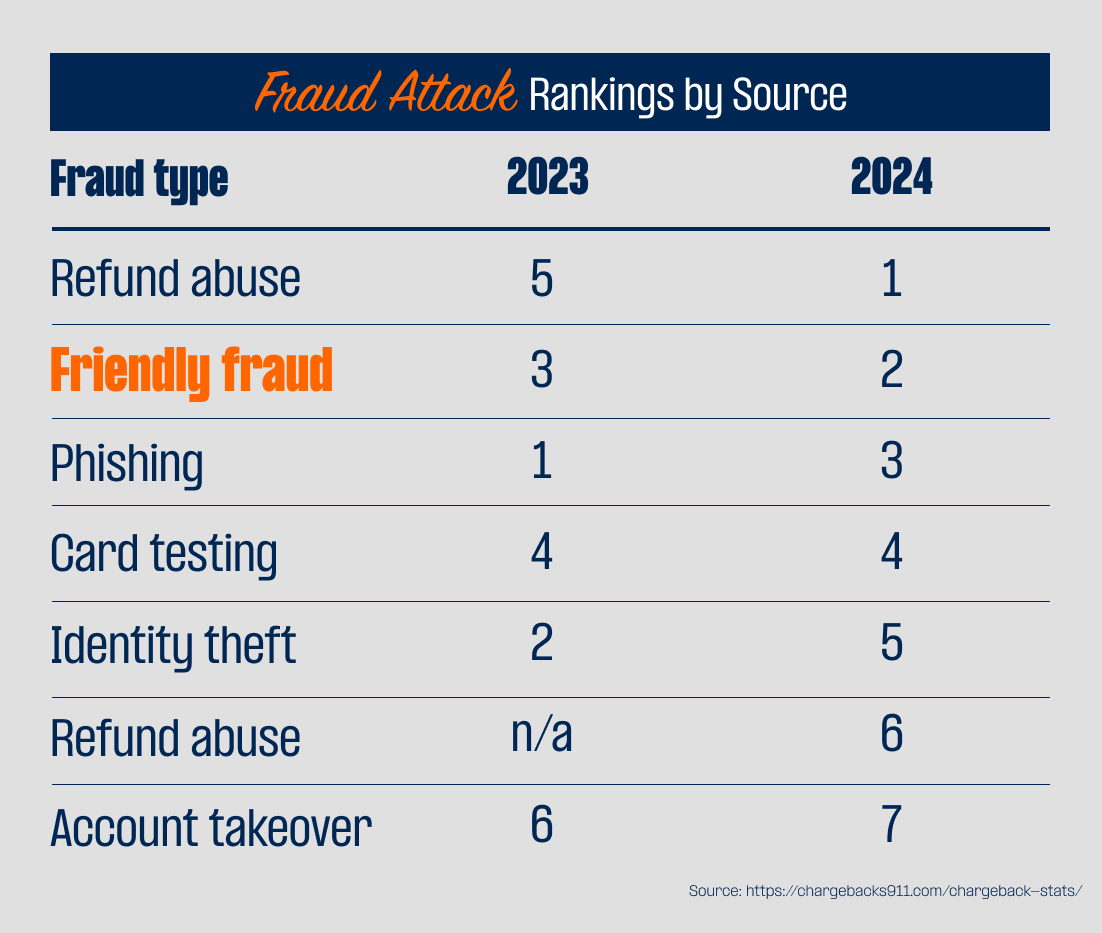

It’s known in the industry as friendly fraud – a contradiction in terms, because often there’s nothing friendly about it. And when customers dispute real purchases, it not only chips away at profit, but muddies fraud metrics and eats up time that could be spent elsewhere. And this problem is escalating fast. According to Chargebacks911, friendly fraud has now become one of the leading fraud attacks against merchants.

Friendly fraud is on the rise

So, what exactly is this kind of fraud? It’s when a customer makes a legitimate purchase and later disputes the charge as fraudulent, usually after receiving the goods and/or services paid for. Occasionally, it’s a genuine misunderstanding: perhaps a shared debit or credit card, a forgotten subscription or an unrecognized name on a statement. But unfortunately, in most cases, it’s deliberate. A consumer decides to keep the product AND the refund. And it’s happening everywhere.

According to a 2024 survey, 72% of eCommerce merchants experienced a rise in friendly fraud, which now makes up a staggering 60% to 80% of their fraud losses. In fact, six in 10 merchants have reported increases in first-party fraud, and friendly fraud now accounts for up to 70% of all fraud cases, costing the global industry roughly $130 billion annually. For merchants simply trying to provide consumers with good service, those statistics are scary, to say the least. For some, friendly fraud could even put their business in jeopardy.

When we dive a little deeper into the data, we see a troubling shift in consumer behavior behind those numbers. Buyer’s remorse is now the driving force behind over 65% of disputes, with the majority being intentional abuse. Even more concerning, 40% to 50% of friendly fraudsters repeat the behavior within 60 days. The takeaway here is clear - once someone gets away with it, they feel empowered to do it again.

This problem is especially pervasive among younger consumers. Social media has normalized chargebacks as a “financial hack,” with 42% of Gen Z shoppers admitting to committing first-party fraud. They also file 60% of their disputes due to regret over impulse purchases, while millennials are 30% more likely to dispute recurring or subscription charges. Friendly fraud is a plague that’s spreading quickly.

The hidden costs of doing nothing.

Friendly fraud is a double-whammy hit on a merchant. First, there’s financial loss from the goods or services that were provided. And then there’s the operational and resource strain.

Each chargeback costs a merchant an average of $128 when fees, penalties, and admin time are factored in. Those numbers quickly add up, especially for businesses processing a high volume of eCommerce transactions every day. But the damage extends beyond dollars.

Excessive chargebacks jeopardize long-term financial stability and can cause real, lasting damage. They drive up fraud ratios, raise red flags with payment processors and networks, and make life harder for everyone involved. For most merchants, managing chargebacks still means digging through transaction records and aligning them with enhanced data via Visa Compelling Evidence. It’s labor-intensive, and even then, the final decision is largely out of their hands.

With Fiserv’s new Integrated Compelling Data product, the heavy lifting of gathering and organizing evidence is greatly reduced. The platform automatically matches transactions and compiles the data Visa requires, helping merchants proactively demonstrate when a dispute is driven by friendly fraud; before fees, penalties, and revenue losses stack up. This is not about shifting responsibility. It’s about giving merchants a clearer, more consistent way to show what really happened so that issuing banks take responsibility for the transaction.

How Fiserv’s Integrated Compelling Data flips the script

Fiserv has long been at the forefront of helping merchants with dispute management. The current manual process, where merchants provide two matching transactions, already helps fight chargebacks effectively, with clients achieving an impressive 85%-win rate on disputes.

But manual processes can only take merchants so far, as it requires merchants to use resources to do the research. And as fraud volumes rapidly increase, the need for speed, consistency and scalability becomes essential. That’s why automated Integrated Compelling Data is such a powerful tool.

This solution automates, simplifies and accelerates the dispute process. Utilizing Integrated Compelling Data streamlines the process by automating the matching of previous transaction data. This includes key elements such as purchase details, device fingerprints, IP addresses, and delivery confirmations. As a result, it enables the creation of a compelling case for every legitimate transaction, alleviating the need for teams to manually compile and submit evidence.

Meeting the moment with new tech

The pace of commerce is not slowing down, and neither are the challenges that come with friendly fraud. For many teams, the pressure to do more with fewer resources is real, and manual processes can make an already difficult job feel overwhelming. Automation is becoming less about efficiency and more about making the workload manageable. By bringing automation and enriched transaction data together, Fiserv aims to help merchants regain some control in a dispute process that often feels stacked against them.

Fiserv has already supported merchants with self-service dispute tools, and the latest enhancements are designed to ease the day-to-day burden and help teams respond with greater confidence.

Conclusion: Turning data into defense

Friendly fraud may be on the rise, but with the automated Integrated Compelling Data tool, merchants are far from powerless. The right data, applied intelligently, turns every transaction into its own line of defense. Automation amplifies that power, turning a time-consuming burden into a streamlined, revenue-protecting advantage. It’s about winning more, losing less, and protecting your bottom line.

Explore related resources